February 10, 2025

TSX60 Series

Rethinking Executive Share Ownership: What’s Next for the TSX60?

Good governance is fundamental to building trust with shareholders and ensuring alignment between executive decision-making and long-term company performance. Meaningful and effective share ownership guidelines are one key mechanism to reinforce such alignment. This article delves into current and emerging practices among TSX60 companies, explores proxy advisor and governance body guidelines, and summarizes Laulima’s predictions.

Download Laulima's article here

Download Laulima's article here

Rethinking Executive Share Ownership:

What’s Next for the TSX60?

Good governance is fundamental to building trust with shareholders and ensuring alignment between executive decision-making and long-term company performance. Meaningful and effective share ownership guidelines are one key mechanism to reinforce such alignment.

This article delves into current and emerging practices among TSX60 companies, explores proxy advisor and governance body guidelines, and summarizes Laulima’s predictions on the future of share ownership guidelines (SOGs).

TSX60 Share Ownership Guidelines (SOG) Findings

Executive SOGs are universal among TSX60 companies¹. The following summarizes Laulima's recent analysis of the key design features as disclosed in the most recent proxy disclosures.

Prevalence

- 93% of TSX60 companies have SOGs in place for the CEO and/or other Named Executive Officers (NEOs)².

- 77% of these companies also extend such policies below the NEO level, encompassing non-CEO direct reports, VPs, and in some cases, director-level positions.

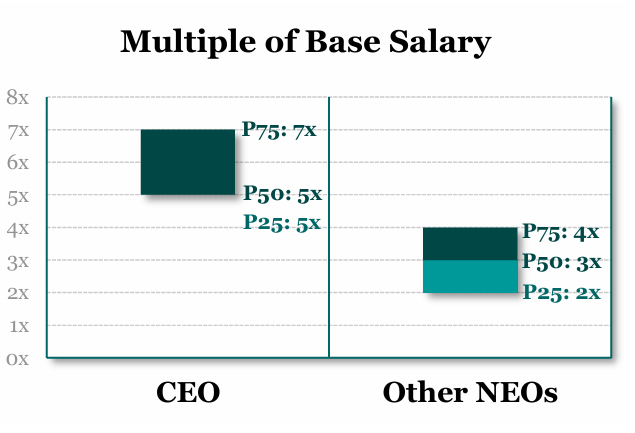

Ownership Multiples

- The majority of companies (91%) express SOGs as a multiple of base salary, although a few companies express SOGs as a multiple of total direct compensation (TDC), long-term incentive (LTI) or as a fixed amount.

- Among companies that denominate SOGs as a multiple of base salary, the median SOG is 5.0x base salary for CEOs and 3.0x base salary for NEOs.

¹ Although statistics in this article are limited to the TSX60, SOGs are also in place for most mid-cap companies, albeit with lower required ownership levels.

² SOGs are less prevalent among companies that are founder controlled and/or have significant insider ownership.

Holding Requirements

- Approximately 40% of TSX60 companies with SOGs have post-employment holding requirements for the CEO and approximately 25% for other NEOs. Most commonly, holding requirements stipulate that minimum ownership levels must be maintained for a period of time following retirement or departure from the company.

- CEOs are required to hold an amount equivalent to their SOG for either 1 year (~65%) or 2 years (~35%). Other NEOs are subject to a 1-year holding requirement in all instances except one, which requires 6 months.

What Counts Towards Ownership

Practice varies among TSX60 companies regarding the inclusion of unvested RSUs, unvested PSUs and unexercised stock options towards compliance with SOGs:

- Unvested RSUs are commonly recognized (~70%), while unvested PSUs are less commonly recognized (~45%) and unexercised stock options are rarely counted (<10%) towards SOGs.

- DSUs are always counted towards compliance in instances where they are used.

Recent Governance and Proxy Advisor Developments

The Canadian Coalition for Good Governance (CCGG)

The CCGG released its recommendations on effective SOGs in 2023. Specifically, the guidance:

- Seeks to promote an economic interest over time by companies enacting an outright common share purchase requirement for CEOs and NEOs. Alternatively, it requires executives use a portion of the proceeds from any vested cash-settled awards to purchase common shares or retain a portion of shares received from vesting of share-settled awards.

- Recommends that SOGs be expressed as a multiple of TDC, rather than base salary.

- Requires the majority of the SOG be met through ownership of common shares, with 75% being “reasonable” and 100% being “ideal”.

- Recommends that if LTI awards count towards SOGs, that they should be limited to awards that have vested, are full value in nature, and that must be held until retirement (e.g. DSUs).

- Expresses that shares should be valued for determining compliance at either market value or the acquisition price, as opposed to valuing at the higher of the two.

Glass Lewis

Glass Lewis clearly stipulates that counting unearned performance-based full value awards and/or unexercised stock options towards SOGs may be viewed as problematic unless compellingly justified. While inclusion of such awards will not automatically lead to an against recommendation on say-on-pay, it is one factor in the proxy advisor’s analysis.

Institutional Shareholder Services (ISS)

ISS does not outline any specific policies pertaining to SOG design features. However, we suspect the proxy advisor will continue to monitor and potentially revisit its voting guidelines in light of the more explicit and prescriptive stances taken by other governance bodies.

The Globe and Mail’s Board Games

Methodology updates released in early 2024 also lend some credence to the CCGG’s recommendations. As of 2024, CEOs are now required to hold 1 to 2 times TDC (dependent on tenure) in company stock for full marks on their annual assessment of governance practices. Previously, CEOs were required to hold 5 times base salary in order to receive the maximum score. Other NEO requirements remain denominated as a multiple (1 to 3 times) of base salary.

Looking Ahead: What Might Change?

Looking ahead, companies will likely review their SOG policies to align with proxy advisor guidelines and emerging governance practices. Based on Laulima’s observations and recent trends, we suspect companies will consider the following:

- Re-assess the inclusion of outstanding LTI towards SOG compliance, with particular scrutiny on PSUs.

- Require a certain portion of SOGs be met in ownership of common shares. While a 50% requirement is common among companies with such thresholds, it is less certain if companies will invoke a 75% or greater requirement to align with the CCGG.

- Review the mix and settlement method of LTI to facilitate SOG attainment.

- Express SOGs as a multiple of TDC to more closely align with emerging guidance. Alternatively, disclosure may be updated to include the executives’ holdings as a multiple of TDC in spite of the SOG still being denominated as a multiple of base salary.

For more information, contact us at info@laulimaconsulting.com.

Lire plus d'articles

VOIR TOUT

.svg)

Dropdown