June 23, 2026

Executive Rewards

How Executive Pay Practices Differ Between Public & Private Companies

We are often asked “How should a private company approach executive compensation?” The reality is that privately-held companies also compete with publicly-traded companies for executive talent, making it valuable to understand how public companies approach executive pay design.

Download the article here

Download the article here

Introduction

Private companies face less external pressure to conform to standardized market norms. They have different structural realities, including the absence of a readily observable share price, limited liquidity, and possibly less access to equity. Private companies may also be more profit-oriented in their pay design. As a result, their practices may differ meaningfully from those of public companies. The answer to this question is not always to mirror public practices, but to understand the unique differences, so compensation can be designed to align with company size, structure, and strategy.

This article outlines how compensation design may differ between public and private companies, and where private organizations can take a more intentional approach – from governance and equity alternatives to performance measurement and market positioning. Understanding this is critical not only to compete for talent, but to deploy compensation strategically as private companies scale.

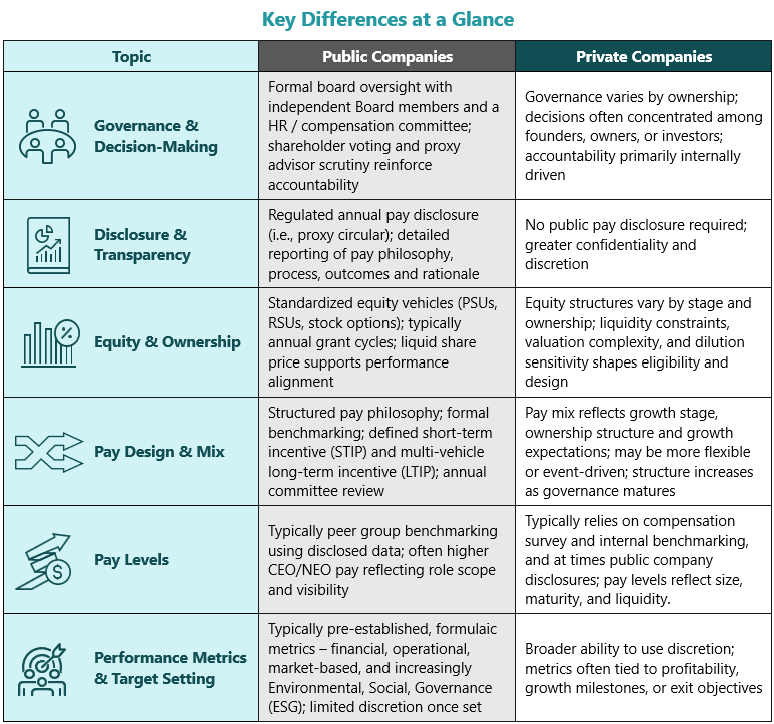

Governance & Decision Making

Public companies operate within a structured framework, with oversight from independent directors and HR / compensation committees that provide objective review. Shareholder voting on director elections and say-on-pay adds a further layer of accountability, while proxy advisors such as Institutional Shareholder Services (ISS) and Glass Lewis apply ongoing scrutiny through evolving evaluation frameworks. Together, these mechanisms impose discipline and create a clear expectation that executive pay must be aligned with shareholder interests and performance outcomes.

Private companies operate with greater flexibility, without the same governance standards that apply to public companies. Compensation decisions are often made by a smaller group of founders, owners/investors or senior executives, who ensure pay aligns with strategy, sustainable performance, and/or long-term value creation. This flexibility can be a strength but also introduces risk. Without clear guardrails, pay decisions can become inconsistent or misaligned with the business.

Private company practices also differ by ownership structure. Investor-backed organizations often align compensation decisions closely to optimal exit objectives, while employee-owned firms may adopt a more structured governance framework to support fair and transparent annual pay decisions. As private companies scale, attract institutional capital, or prepare for an initial public offering (IPO), governance expectations typically increase and begin to resemble public company practices.

Disclosure & Transparency

Public companies are required to disclose executive compensation within the Compensation Discussion & Analysis (CD&A) section of annual proxy circulars. These filings require detailed reporting on pay philosophy, benchmarking approach, performance metrics, and incentive outcomes. This level of transparency subjects compensation decisions to scrutiny from shareholders and proxy advisors, reinforcing discipline in both design and performance alignment.

Private companies are typically not subject to the same public disclosure requirements, which allows for greater discretion and confidentiality. The absence of external guardrails places greater onus on boards and decision-makers, as there is no bright-line standard to guide them. Boards and key decision-makers must establish their own discipline through clear documentation, consistent internal communication, and sound governance practices, particularly as companies grow, attract external capital or compete for senior talent accustomed to public market pay structure and transparency.

Equity & Ownership

Public companies regularly rely on equity vehicles such as performance share units (PSUs), restricted share units (RSUs), and stock options, with participation extended across senior leadership and often broader employee groups. Equity compensation, commonly delivered through the above vehicles, is a fundamental element of public company pay design. Liquidity, transparent share pricing, and direct alignment with the shareholder experience make equity compensation an effective pay-for-performance mechanism. Grants are usually made annually, with vesting and payouts tied to company performance over three to five-year periods.

Proxy advisors closely evaluate these structures, reinforcing expectations around plan design rigour and meaningful executive “skin in the game”. For example, the Canadian Coalition for Good Governance (CCGG) promotes executive share ownership practices such as investing at least 15-20% of total direct compensation (TDC) in common shares, setting share ownership requirements as a multiple of TDC, and requiring these to be met primarily through direct share ownership.

Private companies face a more complex set of considerations when designing equity compensation. Vehicles may include stock options, phantom equity, or other tailored arrangements, with grant frequency and structure varying depending on company stage, ownership type, and the potential for a future liquidity event. LTIP outcomes can be more variable and frequently tied to specific value creation events such as a liquidity transaction or specific milestones, where payouts may be significant, limited, or not realized at all.

Design also varies by ownership structure or stage of growth. In early-stage or founder-led companies, equity may be concentrated among a small group of executives, with stock options used to preserve cash and provide upside. Venture-backed companies often design equity with a defined investment horizon in mind, aligning vesting or performance conditions to growth milestones and anticipated exit events. Established investor-backed firms may tie equity more explicitly to key financial growth objectives. Private companies preparing for a sale of IPO may adopt more structured, performance-based equity frameworks that begin to resemble public company practices.

Pay Design & Mix

Public companies typically apply a structured pay mix grounded in a formal compensation philosophy and market benchmarking. Executive pay is informed by benchmarking against defined peer groups (often targeting median pay levels), incentive programs use clear and formulaic performance metrics, and LTIPs may include multiple equity vehicles. Pay programs are reviewed annually and approved by the HR / compensation committee, with deliberate attention to the balance between fixed and variable pay, performance alignment, and retention and recruitment priorities.

For private companies, there is greater variability. Pay mix often reflects ownership realities and stage of the business, and may evolve over time. Practices are generally less formalized. Founder-led or family-owned businesses may place greater emphasis on salary and discretionary bonuses, and LTIP is less prevalent. Early-stage companies may offer below-market cash compensation but meaningful equity, delivered through front-loaded or milestone-driven LTIP awards aligned with anticipated growth or exit opportunities. Investor-backed organizations may have competitive cash compensation and LTIP tied to a future liquidity event. As companies scale and mature, compensation practices often begin to align with public company principles.

Pay Levels

Public companies may anchor pay levels to a defined, board-approved peer group, comprising of other public companies of similar size, industry, geography, and operating profile. Pay benchmarking relies on publicly-disclosed compensation data from proxy circulars. Decisions are informed by shareholder and proxy advisor perspectives and often reviewed by independent compensation advisors.

Public companies tend to pay more, particularly at the executive levels, reflecting broader stakeholder accountability and the regulatory complexity of operating as a public company.

Private companies more commonly rely on third-party compensation surveys, blended data sources, and internal comparators to inform pay decisions. Survey data can provide useful directional guidance, but it may lack context around ownership structures or company-specific dynamics. While pay levels could be lower than public companies, private companies may choose to pay at or above public benchmarks when required to attract or retain key talent. Ultimately, pay levels are driven less by ownership and more by company scale, market for talent and strategic priorities.

Performance Metrics & Target Setting

Public companies typically adopt formulaic, or largely formulaic, incentive frameworks with pre-established performance metrics approved by the HR / compensation committee and the board at the beginning of the performance period. STIP and LTIP commonly incorporate financial measures, operational or strategic objectives, and market-based metrics such as total shareholder return (TSR) and increasingly ESG measures. These measures are externally visible, benchmarked against peers, and aligned with shareholder and proxy advisor expectations. While boards retain discretion to adjust outcomes, any exercise of discretion is expected to be clearly explained and documented to maintain credibility and stakeholder confidence.

Private companies demonstrate wider variation in approach. Incentive frameworks may be simpler, with a stronger emphasis on financial metrics tied to profitability, and there may also be more discretion in determining outcomes.

In founder-led and family-owned businesses, incentive outcomes tend to rely more heavily on profitability with outcomes determined in a less formulaic way. Investor-backed companies tend to adopt highly measurable, financially driven metrics aligned to growth, return on investment, or defined exit objectives.

Although private company incentive plans can allow for greater flexibility, many companies introduce structured metrics and defined payout ranges over time, to support consistency, comparability, and credibility.

Closing Thoughts

Executive compensation is more than just a cost. It is a strategic enabler of leadership alignment, performance, and long-term value creation. While the ownership model may shape design decisions, other factors such as maturity, governance, capital structure, and strategic goals are equally important inputs to pay decisions. Public companies tend to anchor decisions in market practice and defensibility, given the need to withstand public scrutiny. Private companies have greater flexibility, and with this comes the responsibility to ensure compensation is clearly aligned with company priorities.

There is no “one-size-fits-all” model. Effective design requires applying the right balance of structure, discipline, and flexibility based on the company’s context, reflecting both where the business is today, and where it is going.

Ultimately, compensation sends a signal. The key question is whether it reinforces the behaviours, outcomes, and value creation the organization is aiming to achieve.

If you're exploring how to tailor your executive compensation strategy to reflect your ownership model, growth stage, or evolving talent priorities to stay competitive in today’s market, contact us at info@laulimaconsulting.com.

Read more articles

SEE ALL

.svg)

Dropdown